Module 17: CITIZEN ACTION CARD, Trace A Donation In Ten Minutes

How To Walk A Cascade From Source To Final Grant — And Then Run The Same Trace On Any Large Grant In Your Own County

CITIZEN ACTION CARD — Module 17: Trace A Donation In Ten Minutes

Shadow Patriots Action Library · Project Milk Carton

Pairs with Module 17: “The One Point Six Billion Dollar Donation You Never Voted On” — Marble Freedom Trust / Leonard Leo network

Module 17 walks the architecture of the largest single political-adjacent gift in United States history — Barre Seid’s one point six billion dollar donation of Tripp Lite to Marble Freedom Trust in twenty twenty-one. The architecture is legal. The architecture is structurally inevitable under current rules — the shape is the rules. The trace audit on Module 17 is the move that converts the diagnosis into a skill the citizen can use in their own zip code.

Module 16’s audit (read a fiscal sponsor’s 990 in ten minutes) taught the scale, compensation, related-organizations, grants-paid, self-dealing flags approach. Module 17’s audit extends that skill in one direction: tracing the cascade. Where does a dollar come from? Where does it go after the first entity disburses it? How many hops are there before the dollar arrives at a program grant? Each hop adds one layer of separation between the original donor and the final program output. The number of hops is itself the diagnostic finding.

The trace takes ten minutes. The product is a hop-by-hop public-record map of one cascade. The reader who runs this trace once on the Marble Freedom Trust network can then run the same trace on any donation, any nonprofit, any zip code in the United States. Same template. Same five-field output. Same ten minutes.

The skill is portable. The skill is the product.

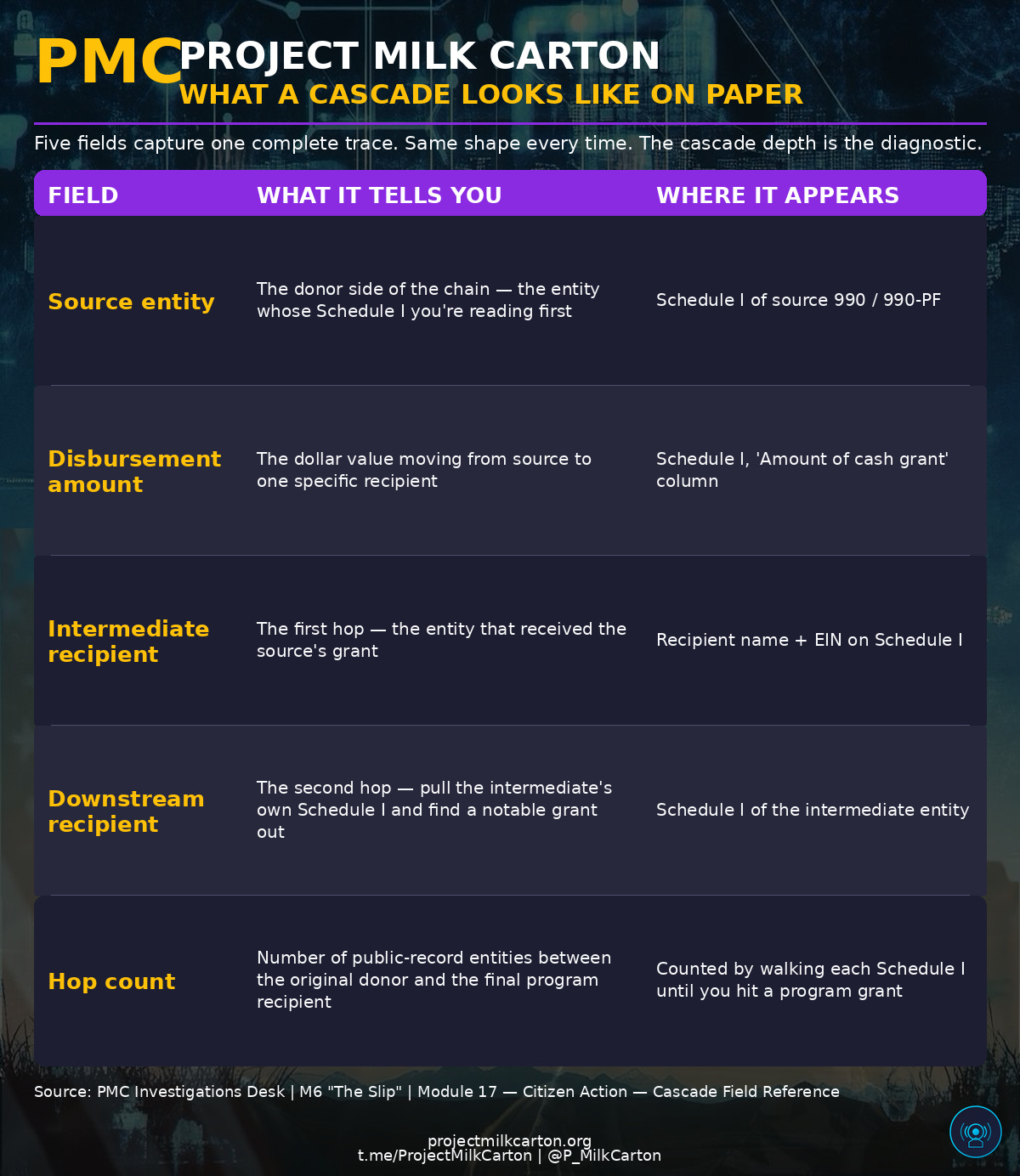

What A Cascade Looks Like On Paper

Five fields. Trace one complete chain. The cascade’s depth is the diagnostic.

The 10-Minute Cascade Trace

Step 1 — Pull the source 990 (1 minute)

Open ProPublica Nonprofit Explorer at projects.propublica.org/nonprofits.

For Module 17, start with Marble Freedom Trust. Search the entity by name; ProPublica returns the trust’s profile with its filed 990-PF documents.

Confirm on the profile page:

The entity’s IRS classification: 501(c)(4) for Marble Freedom Trust

The trust’s most recent fiscal year (filings typically lag 12-18 months)

Click the most recent 990-PF. ProPublica displays it in a structured viewer; you can also download the original IRS-filed PDF.

Step 2 — Find Schedule I (2 minutes)

Marble Freedom Trust files Form 990-PF (private foundation form). Schedule I — grants and contributions paid — lists the entity’s grant recipients for the fiscal year.

Scroll Schedule I (or the equivalent section on a 990-PF). Each row contains: - Recipient name - Address (sometimes) - Recipient EIN (Employer Identification Number — the IRS’s unique entity identifier) - Cash grant amount - Description (often vague — a frequent disclosure gap)

Note the top five recipients by dollar amount. For Marble Freedom Trust, those will include entities you’ll recognize from the article — Schwab Charitable Fund, Concord Fund, the 85 Fund (via Schwab passthrough), DonorsTrust, Knights of Columbus.

Write the top five on your notepad as: name, EIN, amount.

Step 3 — Pick one recipient and pull its 990 (3 minutes)

This is the trace move. Pick one of the top recipients — start with whichever one looks most like a passthrough (e.g., Schwab Charitable Fund or DonorsTrust — DAFs are by design passthrough vehicles).

Go back to ProPublica’s search bar. Search for that recipient by name or EIN.

ProPublica returns the recipient’s own 990 filings. Click the recipient’s most recent 990 — the one that covers the fiscal year matching the original Marble Freedom Trust disbursement (typically the same year or one year later, accounting for fiscal-year timing).

You are now reading the intermediate’s filing. The source dollar from Marble Freedom Trust — assuming it landed inside the intermediate’s fiscal year — is now part of the intermediate’s revenue. The intermediate’s Schedule I shows where the intermediate sent its dollars outward.

This is hop 2 of the trace.

Step 4 — Walk the next hop (3 minutes)

On the intermediate’s Schedule I, find the largest single grant the intermediate made. Note it.

In Marble Freedom → Schwab Charitable case, the next hop will likely be the 85 Fund (or a similarly sized policy / political entity). The 85 Fund receives a substantial portion of what Schwab Charitable passes through.

Note on your notepad: source → intermediate → next-hop. Three entities. Two hops counted.

Now ask the question the audit produces: does this next-hop entity make grants outward, or does it run programs directly?

If the next-hop runs programs (campaign ads, policy reports, conferences), you have reached the program level. Two hops total in this branch. The cascade ended here.

If the next-hop makes grants outward, walk one more hop. Pull the next-hop’s Schedule I and find ITS largest grant out.

Count the hops as you go. Most cascades terminate within 2-4 hops. Some cascades are deeper.

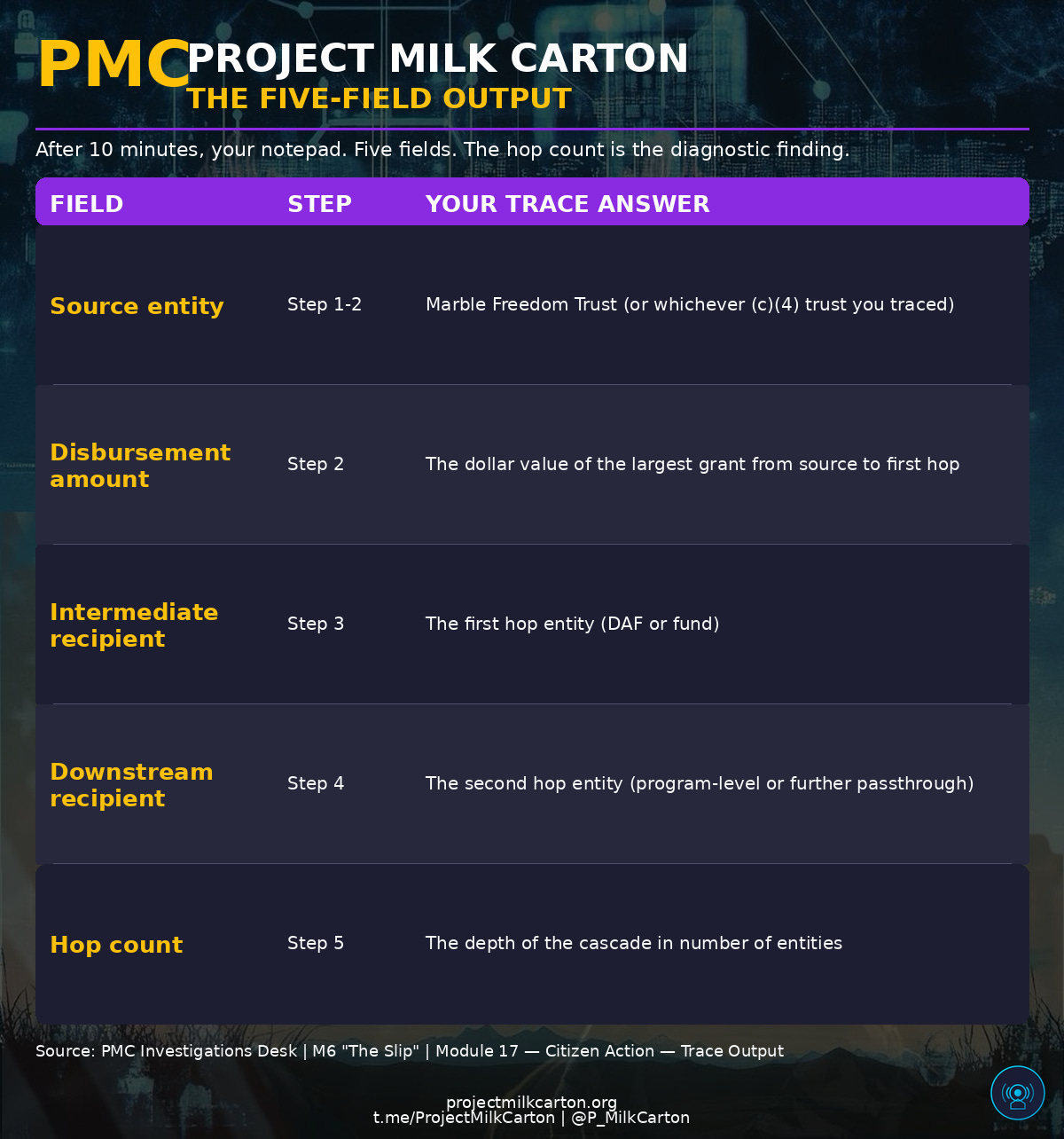

Step 5 — Document the trace (1 minute)

You now have a hop-by-hop map. Write it on your notepad as:

SOURCE: [name] ($[amount] disbursed FY[year])

↓

HOP 1: [intermediate name + EIN]

↓ ($[amount] passed onward to)

HOP 2: [next entity name + EIN]

↓ ($[amount] passed onward to)

HOP 3: [next entity OR “program output — campaign ads / policy work / etc.”]

TOTAL HOPS: [count]

DAYS BETWEEN SOURCE FISCAL YEAR AND FINAL HOP FISCAL YEAR: [estimate]

Take screenshots of each Schedule I you visited. Save them privately. You now have a documented trace.

The Five-Field Output

That’s the five-field map. The map is the literacy.

Now Run It On A Donation In Your Own County

This is where the audit matters most.

Pick any large grant or donation announcement in your own county or state. Local newspapers report on major nonprofit gifts routinely. A foundation gave the local hospital five hundred thousand dollars. A donor-advised fund gave the local arts council two hundred thousand dollars. A family foundation gave the community development corporation one million dollars.

Pick one. The trace takes the same ten minutes.

Source identification: the foundation or DAF making the announced gift

Source’s Schedule I: does this donor regularly grant to your local nonprofit, or is this a one-time gift?

Recipient’s revenue picture: how much of your local nonprofit’s annual revenue does this single gift represent? (Schedule I of the donor vs. Page 1 total revenue of the recipient)

Recipient’s own grants out: does the local nonprofit redirect any of this money to other entities? (Recipient’s own Schedule I)

Hop count: for a local gift, hop count is often 1 (direct donor → program recipient) or 2 (donor → community foundation → program recipient). Higher hop counts in a local context are unusual and worth noting.

The trace skill at the local level tells you whether your community’s nonprofit ecosystem is a direct-grant ecosystem (donors to programs in one or two hops) or a passthrough ecosystem (donors via community foundations or DAFs through multiple hops before reaching programs).

Either pattern can be appropriate. The audit teaches you to see which one you’re looking at.

What The Trace Tells You

The hop count itself is the diagnostic finding.

1 hop (donor directly funds program): the simplest architecture. The donor and the program recipient are publicly linked on a single Schedule I row.

2 hops (donor → DAF or community foundation → program): one layer of passthrough. The donor’s identity is one layer behind the program. This is the standard contemporary American philanthropic architecture for donors who want some anonymity or distribution flexibility.

3 hops (donor → DAF → intermediate fund → program): two layers of passthrough. The donor’s identity is two layers behind the program. The Marble Freedom Trust → Schwab Charitable → 85 Fund cascade is a clear example.

4+ hops: unusual outside of large-scale political-adjacent operations. Each additional hop adds one layer of separation between donor and program and one layer of disclosure complexity.

None of these hop counts is illegal. All of them are allowed. The audit teaches you to recognize which one you are looking at, so when you read a news story about a donation or a grant, you can ask the right question: “How many hops between the donor and the program? And what does the hop count tell me about what the donor and the architects of the cascade prioritized?”

A Reminder About What This Card Is NOT

This card is not a guide to identifying fraud. The 990 filings are tax-compliance documents. Fraud requires undisclosed transactions or misrepresented program expenditures — neither of which a Schedule I trace reliably detects on its own. Fraud detection requires forensic accounting. The trace is for understanding legal architecture, not for accusing entities of illegality.

This card is not a guide to public attack on donors or trustees. Naming a donor on social media as the source of a cascade is rarely useful and often counterproductive. The donor used legal vehicles and disclosed where the law required disclosure. The audit produces a citizen who can read the cascade, not a citizen who reposts cascade fragments out of context. The Shadow Patriots map. We do not expose. The map is for you.

This card is not a substitute for asking direct questions. If a local trace surfaces something you find concerning about a nonprofit in your county, the nonprofit’s annual report, public communications, and direct outreach channels often answer the question more clearly than the 990 alone. Most nonprofits welcome questions from informed citizens — and informed is the operative word. The trace is what makes you informed before you ask.

Quick Reference — Where Things Live On A 990 (Recap From Module 16)

Page 1 summary — total revenue, total expenses, net assets, governing body count

Part VII — officer compensation (Section A) + top five compensated employees (Section B)

Schedule A — public charity status verification (501(c)(3) only)

Schedule B — Schedule of Contributors. (c)(4) Schedule B is filed but redacted from public-record copies — the Module 10 vault.

Schedule I — grants paid out to U.S. organizations and individuals. This is the trace schedule.

Schedule J — supplemental compensation information for officers

Schedule L — transactions with interested persons (self-dealing disclosure)

Schedule R — related organizations (the architecture map)

For 990-PF filings (private foundations and some trust forms): - The grants paid section serves the equivalent function to Schedule I - Required investment income disclosure - Distinct calculations for minimum distribution requirements

After The Trace

The trace produces a reading skill. The reading skill produces a citizen. The citizen has options.

The Shadow Patriots do not tell readers what to do with the literacy. Some readers will: - Show the trace to a journalist as a tip — most local outlets welcome trace-audited tips - Ask their local nonprofit board members questions about cascade depth at a public board meeting - Apply the trace skill before donating to any large fund or foundation in their orbit - Use the trace to identify which local programs are downstream of which large donors — useful intelligence for any community-development decision - Teach the trace skill to one other person who has been wondering “where does the money actually come from”

The literacy lives in the citizen regardless. The next time someone tells you “a foundation funded this initiative,” you can ask the next question: “Which foundation, what’s their Schedule I look like, and what’s the cascade depth?”

The Tool

Every entity in this trace — Marble Freedom Trust, Schwab Charitable Fund, the 85 Fund, Concord Fund, DonorsTrust, Knights of Columbus, and every nonprofit in your county — was operated by people who showed up. The 990 filing is a tool. ProPublica Nonprofit Explorer is a tool. The five-field cascade trace is a tool.

Tools do not pick sides. The side that shows up owns the tool. If you do not show up, someone else will — and they may not have your town in mind. Will they have the safety of your children in mind?

The citizen who traces a cascade ending in a youth-services nonprofit in their county is doing the citizen’s part of the work the architecture was built to operate around. The 990 is one of the few documents the architecture cannot redact, rebrand, or route around. The cascade is the architecture’s most public surface. The trace is the participation the rules permit.

Shadow Patriots Action Library · Module 17 · Project Milk Carton · 501(c)(3) · EIN 33-1323547

Evidence standard: every claim in this card is verifiable through publicly filed 990s and the public-record tools named (ProPublica Nonprofit Explorer, IRS Tax Exempt Organization Search). No private information required. No allegation of misconduct required. The trace’s product is the citizen’s literacy. The citizen’s choice of what to do with the literacy is theirs.

Editorial discipline (Tier 1 financial doctrine): Named legal entities (Marble Freedom Trust, Schwab Charitable Fund, the 85 Fund, Concord Fund, DonorsTrust, Knights of Columbus) are permitted because the symmetry between M16 and M17 entities IS the teaching. Where individuals are named — Barre Seid as donor, Leonard Leo as trustee — they are named in the structural roles they hold under public filings. The trace teaches the same skill regardless of the entities’ politics. The skill is the product. The architecture is the diagnosis. The citizen is the destination.