Module 16: CITIZEN ACTION CARD, Read A Fiscal Sponsor’s 990 In Ten Minutes

How to Audit A Nonprofit’s Filing Stack — And Then Run The Same Audit On A Nonprofit In Your Own County

CITIZEN ACTION CARD — Module 16, Read A Fiscal Sponsor’s 990 In Ten Minutes

Shadow Patriots Action Library · Project Milk Carton

Pairs with Module 16: “The Engine That Looks Like Seven Engines” — Arabella Advisors / Sunflower Services

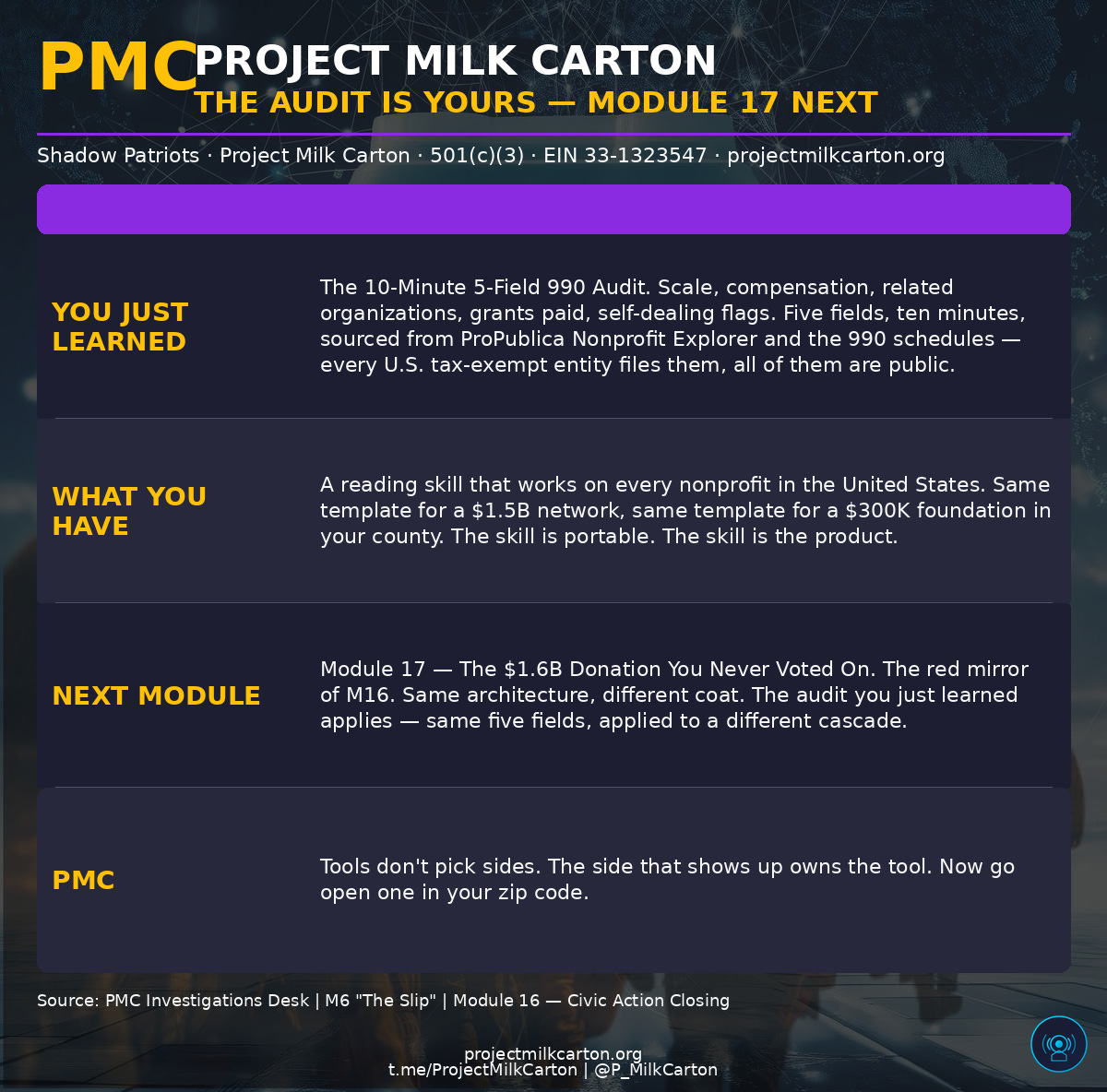

Module 16 walks the architecture of a $1.5 billion-a-year network of seven nonprofits managed by a single firm. The architecture is legal. The architecture is mirrored on the opposite political coat (Module 17 walks that mirror). The architecture is structurally inevitable under current rules — the shape is the rules. The audit on Module 16 is the move that converts the diagnosis into a skill the citizen can use in their own zip code.

The audit takes ten minutes. The product is a five-field public-record artifact identifying who runs the entity, where the money flows, and who pays whom for what. The reader who runs this audit once on the Arabella network can then run the same audit on any (c)(3) or (c)(4) in any zip code in the United States — same template, same five-field output, same ten minutes.

The skill is portable. The skill is the product.

What A 990 Tells You

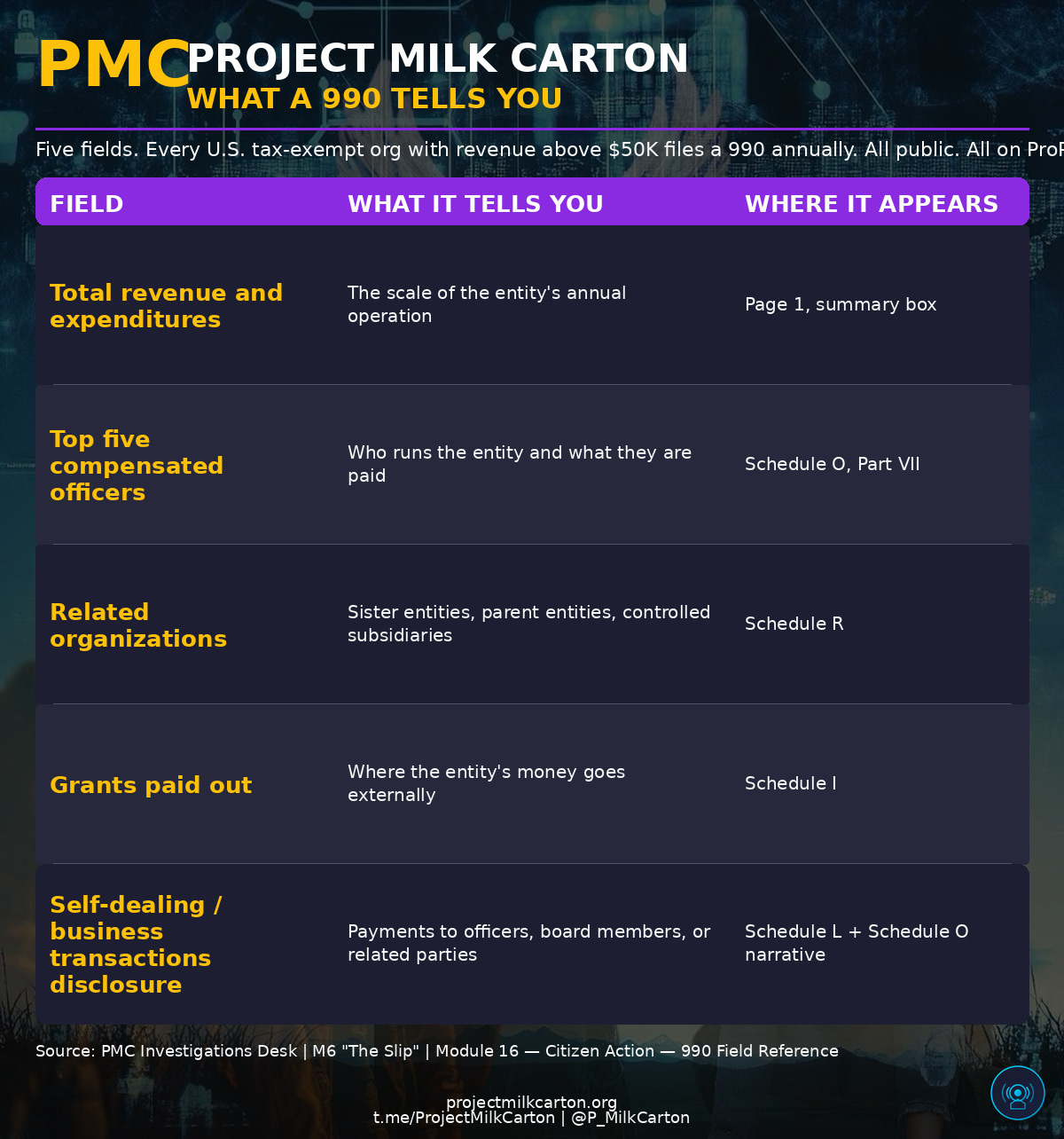

Every U.S. tax-exempt organization with revenue above $50,000 files an IRS Form 990 annually. The 990 is a public document. It contains the entity’s revenue, expenditures, top compensated officers, related organizations, grants paid out, contracts paid to vendors, and narrative answers about its operations. Most of the architecture this series describes is visible on the 990 — once the citizen knows where to look.

The audit pulls the five fields below from a single 990. Together they form a structural map of the entity. The same five fields work on every nonprofit in the United States.

Five fields. Ten minutes. The reader who fills in the five fields knows more about the entity than 99% of people who have ever heard the entity’s name.

The 10-Minute 990 Audit

Step 1 — Pull the 990 (1 minute)

Open ProPublica Nonprofit Explorer at projects.propublica.org/nonprofits.

In the search bar, type the entity’s exact name. For Module 16, start with New Venture Fund — the largest of the seven Arabella-managed entities and the largest fiscal sponsor in the United States.

ProPublica returns a profile page for the entity. The profile shows the entity’s EIN, address, mission classification, and a list of the most recent 990 filings. Click the most recent 990 filing. ProPublica displays the 990 in a structured viewer; you can also click “Download PDF” to pull the original IRS-filed document.

Confirm two things on the profile page before you proceed:

The entity’s IRS classification: 501(c)(3) public charity, 501(c)(3) private foundation, 501(c)(4) social welfare organization, or other category. (New Venture Fund is a (c)(3) public charity.)

The entity’s most recent fiscal year. Most 990s lag the calendar year by 12-18 months — a 990 you pull in 2026 typically reports fiscal year 2024.

You now have the 990 in front of you. The next four steps walk the five-field audit.

Step 2 — Read Page 1 (1 minute)

Page 1 of every 990 contains a summary box. The summary box is unmissable — it occupies the top half of the first page.

Note the following four numbers:

Total revenue for the fiscal year

Total expenses for the fiscal year

Net assets / fund balance, end of year

Number of voting members of the governing body

Write these on your notepad as your “scale” line.

For New Venture Fund, the most recent fiscal year’s total revenue is in the high nine figures. The expense figure tracks revenue closely — fiscal sponsors typically operate near revenue-neutral on annual basis because the money flows through to projects. The net assets line tells you the entity’s reserves. The governing-body voting-member count tells you how many people, in formal governance terms, control the entity.

Step 3 — Read Schedule O / Part VII (2 minutes)

Schedule O is the 990’s narrative attachment. It contains long-form answers to disclosure questions. Part VII of the main 990 lists the entity’s officers, directors, key employees, and the five highest-compensated employees who are not officers.

Note the following:

Names and titles of the top five compensated employees. (Officers and key employees are in Section A; the five highest non-officer employees are in Section B.)

Reportable compensation from the entity for each.

Reportable compensation from related organizations for each.

This column is the audit money column. If a top employee receives compensation from the entity AND a related organization, you are looking at personnel overlap — the move Module 9 walked.

For an Arabella-managed entity, you will see senior personnel whose total compensation includes both an entity-level salary and additional compensation from a related organization. The related organization is typically Arabella Advisors (the consulting firm) or one of the other six Arabella-managed nonprofits. The personnel overlap is on the 990. The 990 is public. The overlap is legal under current rules. The disclosure of the overlap is what you are looking at.

Step 4 — Read Schedule R (3 minutes)

Schedule R lists related organizations. It is the most analytically valuable schedule on the 990 for the Module 16 audit.

Schedule R has multiple parts:

Part I: Identifies disregarded entities (entities the IRS treats as part of the filing nonprofit).

Part II: Identifies related tax-exempt organizations (other nonprofits the entity controls or is controlled by).

Part III: Identifies related organizations taxable as partnerships.

Part IV: Identifies related organizations taxable as corporations.

Part V: Reports transactions with related organizations — this is the audit transactions section.

For the Module 16 audit, focus on Part II and Part V.

Part II for New Venture Fund will list the other Arabella-managed entities (Sixteen Thirty Fund, Hopewell Fund, Windward Fund, North Fund, Telescope Fund, Impetus Fund) AND Arabella Advisors itself. The relationship column will describe the structural relationship — typically “shared management” or “common officers.” This is the box-and-arrow of the architecture made literal on the filing.

Part V lists the dollar value of transactions between the filing entity and the related entities. For an Arabella-managed entity, you will see line items for management fees paid to Arabella Advisors, and possibly for grants given to or received from sister entities. The management fees are the line you are looking for.

Write down on your notepad:

The list of related organizations (the seven entities + the management firm)

The total dollar value of management fees paid to the management firm in the fiscal year

Any grants paid out to or received from sister entities

You now have the structural map of the architecture’s transaction flow.

Step 5 — Read Schedule I (3 minutes)

Schedule I lists grants the entity paid to other organizations. It is the most analytically valuable schedule for tracing money downstream.

Schedule I has two parts:

Part II: Grants to U.S. organizations and governments.

Part III: Grants to U.S. individuals.

For New Venture Fund, Schedule I Part II will list dozens to hundreds of grant recipients. Each row contains:

Recipient name - EIN (Employer Identification Number — the IRS’s unique entity identifier)

IRC section (the recipient’s tax category)

Amount of cash grant - Description of grant (often vague — a frequent disclosure gap)

The audit move on Schedule I is to pick three to five recipient organizations that catch your eye and look them up. Two reasons one might catch your eye:

You don’t recognize the name. That is the most common reason an entity is on a fiscal sponsor’s Schedule I — it’s a hosted project that does not appear in IRS records as an independent organization. Look up the name. If ProPublica returns no separate 990 for that entity, you have just identified a fiscal-sponsorship project — a move Module 5 walked.

The grant amount is unusually large or unusually small. Large amounts often go to peer institutions or to specific high-priority program areas. Small amounts can indicate seed grants, sub-grants, or pass-through pieces of larger transactions.

For each of the three to five recipients you check, write down on your notepad: name, EIN, grant amount, and whether the recipient appears as a separately filed 990 entity or only as a fiscal-sponsorship project.

You now have a downstream map of where the entity’s money flowed externally in the fiscal year.

The Five-Field Output

After ten minutes, your notepad contains:

Anything in Schedule L or Schedule O narrative that discloses payments to officers, board members, or controlled parties

That’s the five-field map. The map is not an accusation. The map is a structural description of the entity’s operating architecture. The map shows you, in IRS-filed prose, what the entity does, who runs it, and where its money goes.

The map is the literacy. Once you have run the audit on one entity, you can run it on any entity. The schedules are the same on every 990. The audit moves are the same on every audit. The five-field output is the same shape every time.

Now Run It On A Nonprofit In Your Own County

This is the move that matters most.

Pick a nonprofit in your own zip code or your own county. Any nonprofit. The nonprofit’s name appears on a tax form, a fundraising letter, a billboard, a school program, a sports league, a youth-services advertisement, a hospital wing, an arts council, or a community development corporation. Pick one. The audit takes the same ten minutes.

The audit on a local nonprofit produces information no marketing material can disguise:

Scale tells you whether the nonprofit’s actual operating budget matches its public profile.

Compensation tells you whether the executive director is paid more than the local school superintendent — a defensible figure in many cases, a notable figure in some.

Related organizations tells you whether your local nonprofit is part of a larger network or a standalone entity.

Grants paid tells you whether the nonprofit’s program spending matches its fundraising claims.

Self-dealing flags tells you whether any officer or board member has a financial transaction with the nonprofit beyond their disclosed compensation.

Five fields. Ten minutes. Same template. The skill is portable across all 1.8 million tax-exempt organizations in the United States.

The architecture Module 16 describes is a bigger version of the architecture in your county. Not because Arabella is in your county. Because the same legal vehicles — (c)(3), (c)(4), DAFs, fiscal sponsorship, related-party transactions, management fees — operate at every scale. The skill that audits a $1.5B network audits a $300K local foundation with no modification.

What The Audit Tells You

Once you have run the audit on three or four entities — one Arabella-managed entity, one Marble Freedom Trust-related entity (after Module 17 lands), and one or two nonprofits in your own county — you will start spotting the structural shape on every 990 you read.

The shape: revenue figure, scale of operation, compensation structure, related-organization map, grants-out map, self-dealing disclosures. Once you know the shape, the 990 stops being a long opaque document and becomes a structured legal portrait of the entity.

The shape becomes a reflex. You will start noticing things. A small foundation in your county that pays its director four hundred thousand dollars on a five hundred thousand dollar budget. A “youth services” nonprofit whose Schedule I grants flow primarily to its own related organizations. A community development corporation whose Schedule L discloses real-estate transactions with a board member’s company. A faith-based charity whose total grant disbursements amount to less than ten percent of its annual revenue.

None of these patterns is, by itself, a violation. All of them are visible on the 990. The audit teaches you to see them. Seeing them is the literacy.

A Reminder About What This Card Is NOT

This card is not a guide to identifying fraud or wrongdoing. The 990 is a tax-compliance document. Fraud, when it occurs, typically involves either undisclosed transactions or transactions disclosed in misleading ways — neither of which a 990 audit reliably detects on its own. Fraud detection requires forensic accounting, not 990 reading.

This card is also not a guide to public attack on the entities you find. Naming a small local nonprofit on social media is rarely useful and frequently counterproductive. The audit is for you. The audit produces a citizen who can read 990s, not a citizen who reposts 990 fragments out of context. The Shadow Patriots map. We do not expose. The map is for the citizen who runs the audit.

This card is also not a substitute for asking the nonprofit directly. If the audit raises a question, the nonprofit’s annual report, public communications, and direct contact channels often answer the question more clearly than the 990 alone. Most nonprofits welcome questions from informed citizens — and informed is the operative word. The audit is what makes you informed before you ask.

Quick Reference — Where Things Live On A 990

For when you have run the audit a few times and need a quick lookup:

Page 1 summary — total revenue, total expenses, net assets, governing body count

Part VII — officer compensation (Section A) + top five compensated employees (Section B)

Part IX — functional expense breakdown (program / management / fundraising)

Part XI — net asset reconciliation

Schedule A — public charity status verification (501(c)(3) only)

Schedule B — Schedule of Contributors (donors). NOTE: Schedule B is filed with the IRS but redacted from public-record copies for (c)(4) entities and most (c)(3) public charities. The Schedule B vault — Module 10 — is the architecture this redaction is part of.

Schedule G — fundraising activities disclosure

Schedule I — grants paid out to U.S. organizations and individuals

Schedule J — supplemental compensation information for officers

Schedule L — transactions with interested persons (the self-dealing disclosure schedule)

Schedule O — supplemental narrative information (long-form answers to disclosure questions)

Schedule R — related organizations (the architecture map)

After The Audit

The audit produces a reading skill. The reading skill produces a citizen. The citizen has options.

The Shadow Patriots do not tell readers what to do with the literacy. Some readers will:

File a public-records request to a nonprofit they audited (most state attorneys general accept charitable-trust complaints from any citizen).

Bring the audit findings to a local journalist as a tip — most local outlets welcome tips that come pre-audited.

Show up at a board meeting of a local nonprofit they audited and ask informed questions.

Apply the audit skill before donating, volunteering, or engaging with any nonprofit in their orbit.

Teach the audit skill to one other person — a spouse, a neighbor, a friend, a kid old enough to read a column of numbers.

Some readers will run the audit once and then never run it again. The literacy lives in the citizen regardless. The next time someone tells the citizen “this nonprofit serves the community,” the citizen now knows that “serves the community” can mean any of a dozen architectural patterns. The citizen can ask the next question.

That is the product. The audit is for getting the literacy. Once you have it, you do not need to run it again unless you want to.

The Tool

Every entity in this audit — New Venture Fund, Sixteen Thirty Fund, the seven Arabella entities, the management firm itself, and every nonprofit in your county — was built by people who showed up. The 990 is a tool. The IRS Tax Exempt Organization Search is a tool. ProPublica Nonprofit Explorer is a tool. The five-field audit is a tool.

Tools do not pick sides. The side that shows up owns the tool. If you do not show up, someone else will — and they may not have your town in mind. Will they have the safety of your children in mind?

The reader who runs this audit on a youth-services nonprofit in their county is not paranoid. The reader is doing the citizen’s part of the work the architecture was built to operate around. The 990 is one of the few documents the architecture cannot redact, rebrand, or route around. The 990 is the evidence the rules require. The reading is the participation the rules permit.

Shadow Patriots Action Library · Module 16 · Project Milk Carton · 501(c)(3) · EIN 33-1323547

Evidence standard: every claim in this card is verifiable through publicly filed 990s and the public-record tools named (ProPublica Nonprofit Explorer, IRS Tax Exempt Organization Search). No private information required. No allegation of misconduct required. The audit’s product is the citizen’s literacy. The citizen’s choice of what to do with the literacy is theirs.

Editorial discipline (Tier 1 financial doctrine): Named legal entities (the seven Arabella-managed entities, Arabella Advisors / Sunflower Services, donors named in their public-record structural roles) are permitted because the symmetry between M16 and M17 entities IS the teaching. The audit teaches the same skill regardless of the entity’s politics. The skill is the product. The architecture is the diagnosis. The citizen is the destination.