Module 4: The Russian Doll

How a single operator builds a stack of nonprofits, PACs, and LLCs — and why the donor’s money changes identity every time it moves

By the PMC Investigations Desk · Project Milk Carton · Module 4 of “The Game You Were Never Taught” · Financial Move 2 of 8

The move

This is the second of eight financial moves we will map in this series. In Module 3 we showed you how a Donor-Advised Fund erases the donor’s name from a single donation. That is the first move. DAF Stacking gets the money from a named human being into the charitable system without leaving a public fingerprint.

The second move takes the money from there and walks it through a stack.

Entity Laddering is the practice of building a coordinated group of legally separate organizations — typically a 501(c)(3), a 501(c)(4), a political action committee, and one or more limited liability companies — and routing the same donor’s money through the stack to accomplish activities that no single entity on the ladder is legally permitted to do on its own.

The (c)(3) cannot lobby. The (c)(4) can lobby but should not be primarily political. The PAC can be primarily political but must disclose its donors. The LLC does not have to disclose anything, but it cannot accept tax-deductible donations.

Each rung has a different rule. Each rung is run by the same people. The money changes its legal identity every time it crosses a rung. And because each rung is a legally separate entity, no single Form 990 or FEC filing ever tells the whole story.

That is the Russian Doll. Open one doll, and another identical doll is inside it.

How it works — in plain English

Here is the basic sequence. We will use generic labels. In the case studies below we will put real names on the rungs.

Rung 1 — The (c)(3). A tax-exempt educational or charitable organization. Donors deduct their gifts. The organization cannot endorse candidates. It can publish research, run programs, and engage in a limited amount of non-political lobbying.

Rung 2 — The (c)(4). A tax-exempt “social welfare” organization. Donors do not deduct their gifts, but donors do not have to be disclosed publicly. A (c)(4) can lobby without limit and can engage in some campaign activity as long as campaign activity is not its primary purpose.

Rung 3 — The PAC or Super PAC. A political action committee registered with the Federal Election Commission. A PAC can endorse candidates and run election ads directly. A PAC must disclose its donors to the FEC.

Rung 4 — The LLC. A limited liability company. Not tax-exempt. Not regulated by the FEC unless it makes political expenditures. Does not have to disclose members, officers, or ownership in most states — Delaware, Nevada, and Wyoming are the most opaque.

Now the stack.

Step 1. A donor gives to the (c)(3). The gift is tax-deductible. The (c)(3) files a 990 that discloses the top officers and contractors but not the donor (Schedule B is redacted from the public copy).

Step 2. The (c)(3) pays the (c)(4) — for “research services,” “management fees,” “shared overhead,” or a grant. This is legal as long as the (c)(3) is paying for something the (c)(4) actually delivers. On the public 990, this transfer appears as an expense or a grant to a related organization.

Step 3. The (c)(4) now has money it does not have to attribute to any specific original donor. The (c)(4) uses that money to lobby, to run issue ads, and — within limits — to fund election-adjacent activity.

Step 4. The (c)(4) contributes to the PAC or the Super PAC. On the PAC’s FEC filing, the contribution shows up as coming from the (c)(4) — not from the original donor in Step 1. The (c)(4) is the disclosed donor. The (c)(4)’s own donors remain undisclosed.

Step 5. The PAC runs political ads, funds candidates, and pays consultants. The money that started as a tax-deductible gift to an educational nonprofit is now a political expenditure attributed to a social welfare organization.

Step 6. At any step in the chain, the LLC can be inserted. The (c)(4) pays the LLC for “consulting.” The LLC pays vendors. The vendors do the work. The (c)(4)’s 990 shows a lump-sum consulting payment to the LLC. The LLC files no public return. The trail ends.

The donor’s name appears only on the (c)(3)’s redacted Schedule B, which the public cannot see. The activity — the political work, the ads, the candidate support — appears on filings that point back only to the (c)(4) or the LLC. No public document links the donor to the activity.

The money moved. The identity changed at every rung. The work got done. And every rung was legal.

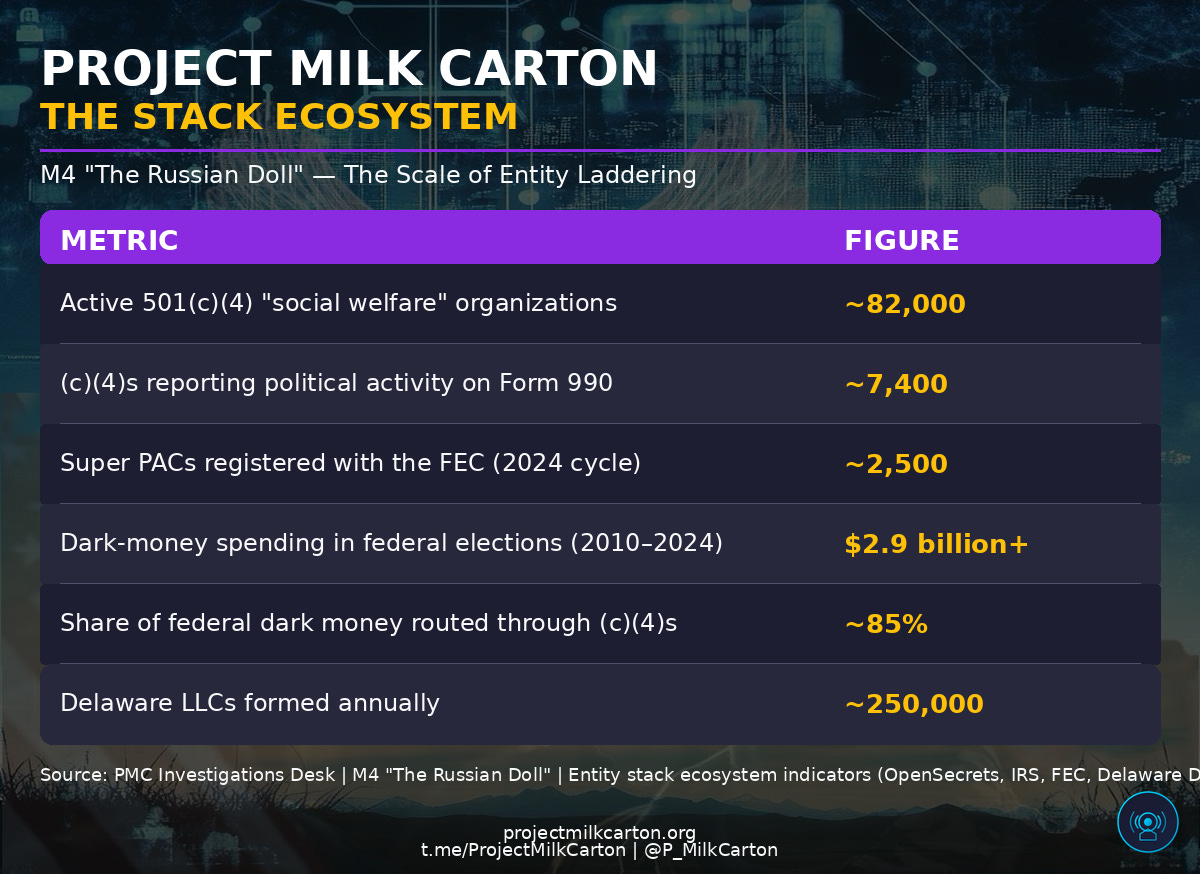

The scale

Entity laddering is not a boutique technique. It is the scaffolding of modern American political and advocacy infrastructure.

Estimates of dark-money spending — money spent on political activity where the original donor cannot be identified from public records — have grown from roughly $69 million in the 2008 cycle to more than $1 billion in the 2024 cycle. The overwhelming majority of that growth came not from new donors, but from the expansion of entity stacks that laundered identity at each rung.

The mechanism scales in both directions. A single operator can build a stack. A coordinated network of operators can build a web — dozens of (c)(3)s feeding dozens of (c)(4)s feeding dozens of PACs, all sharing a back-office staff, a shared address, and a shared set of vendors.

Why this is the second move

Move 1 — DAF Stacking — got the donor’s name off the donation.

Move 2 — Entity Laddering — gets the money into the right regulatory bucket for whatever needs to be done with it.

DAF Stacking alone can fund a straightforward grant to a recognized charity. But DAF money cannot, on its own, be used to run an election ad or fund a lobbying campaign. The money has to move up the ladder. A (c)(3) can receive DAF money. A (c)(4) can receive money from a (c)(3). A Super PAC can receive money from a (c)(4). By the time the money reaches the Super PAC, it has been transformed three times — each transformation legal, each transformation a break in the public paper trail.

This is why the two moves work together. DAF erases the donor. Laddering gives the money the legal identity it needs to do political work. Subsequent moves in this series — fiscal sponsorship, foreign principal pass-through, LLC opacity — extend the ladder further, or weld new sections onto it.

The Russian Doll is how the modern influence machine is actually built. Everything else is a variation on it.

There are legitimate uses

Entity laddering, like DAF Stacking, is not intrinsically sinister. There are real structural reasons an organization might run a (c)(3) alongside a (c)(4).

A think tank that publishes policy research (a (c)(3) activity) may have a sister organization that lobbies Congress on the policies the research recommends (a (c)(4) activity). Running those as separate entities is legally required, not deceptive.

A civic organization that advocates on an issue may spin off a PAC to endorse candidates who support that issue. Keeping the PAC legally separate from the (c)(4) is not a maneuver — it is a compliance requirement.

Sierra Club, Planned Parenthood, the NRA, the ACLU, the Heritage Foundation, and hundreds of other household-name organizations operate (c)(3)/(c)(4)/PAC stacks. These stacks are disclosed, the officers are public, the movement of money between entities is auditable on each entity’s 990 and FEC filings.

The technique is legal. It becomes problematic when the stack is designed to break the public paper trail rather than to comply with the compliance requirements that made the stack necessary in the first place. The distinguishing signal is not the existence of the stack. The signal is opacity at the transitions — transfers that do not match any clear program, LLC insertions with no stated purpose, shared officers across entities that publicly disclaim coordination, and donor disclosures that end at the first rung rather than documenting the full flow.

This module will teach you how to look at a stack and tell the difference.

Case Study A — The Judicial Influence Stack

The clearest live example of a tightly laddered stack on the American right is the cluster of organizations associated with a single long-tenured operator in the judicial nomination and influence space. The names have rotated — some organizations have rebranded, some have been wound down and spun back up under new names — but the mechanics have stayed the same for roughly fifteen years.

The stack typically contains:

A 501(c)(3) educational nonprofit that publishes legal research and trains lawyers (donors’ gifts are tax-deductible; donors are not publicly disclosed).

A 501(c)(4) social welfare organization that runs issue ads and lobbies on judicial confirmations (donors are not disclosed at all).

One or more LLCs that the (c)(4) pays large sums to for “consulting” or “strategic services” (LLCs do not file public returns).

A Super PAC that runs election-adjacent advertising in races where judicial issues are salient (donors to the PAC are disclosed to the FEC — but the disclosed donor is often the (c)(4), not the original human donor).

In one recent reporting cycle, a single (c)(4) at the top of this stack received more than $1.6 billion in anonymous donations across a three-year period. Those donations were not deductible. The donors’ names do not appear on any public filing. The (c)(4) then distributed those funds across the rest of the stack in transfers that appear on its own 990 but that do not trace back to any identified individual or institution at the top.

The public-facing work produced by this stack includes substantial advocacy on federal judicial nominations, state supreme court elections, and the confirmation of specific federal judges. The work is legal. The funding architecture is legal. The disclosure architecture is the problem: the work is politically consequential, and the people paying for it are invisible.

This stack is coded red because, in practice, its advocacy has been aligned with conservative judicial and legal causes. The mechanics of the stack are not partisan. The same mechanics appear on the left.

Case Study B — The Pop-Up Nonprofit Infrastructure

Source: PMC Investigation [REDACTED] supplemented by public investigative reporting (ProPublica, Capital Research Center, New York Times, OpenSecrets)

The clearest live example of a tightly laddered stack on the American left is the family of entities managed by a single for-profit consulting firm based in Washington, D.C. This firm functions as the administrative back-office for several large (c)(3)s, (c)(4)s, and associated pop-up organizations.

The stack typically contains:

A small number of flagship 501(c)(3)s that receive grants from major foundations and DAFs (donors are not disclosed on the public 990).

A flagship 501(c)(4) that functions as the primary dark-money political vehicle (donors are not disclosed anywhere).

Dozens of “pop-up” (c)(4) brand names — issue-specific nonprofits created to run a particular advocacy campaign. Many of these pop-ups share an address, a board, a bank account, and a phone number with the flagship (c)(4). They often exist for a single campaign cycle and then go dormant.

Multiple LLCs and independent contractors who receive large consulting payments from the (c)(4) flagship.

Across recent election cycles, this family of entities has moved more than $3.5 billion through the dark-money side of the ladder. The flagship (c)(4) at the top of this stack has ranked repeatedly among the largest single sources of dark-money political spending in the country.

Coverage from both mainstream and investigative outlets has documented the stack extensively: the shared back-office structure, the pop-up (c)(4) brand names, the coordinated messaging, and the absence of publicly disclosed original donors. None of the reporting alleges illegal activity. The activity is legal. The disclosure architecture is the problem.

This stack is coded blue because, in practice, its advocacy has been aligned with progressive causes. The mechanics are identical to the red-coded stack above. The same ladder. The same rungs. The same transitions. The same donor invisibility. Only the political direction differs.

The legal architecture

Three bodies of law intersect to make entity laddering legal.

The Internal Revenue Code defines what a (c)(3), (c)(4), and PAC are allowed to do and how they must file. The code permits transfers between related entities as long as each transfer is for a bona fide purpose and is properly reported on each entity’s Form 990. The code does not require the recipient of a (c)(3) grant from a (c)(4) to trace that money back to its original donor.

The Federal Election Campaign Act governs what a PAC can do and what it must disclose. The PAC discloses its donors — but a donor that is itself an entity (a (c)(4), an LLC, another PAC) is disclosed as the entity. The underlying individuals are not. The act does not require a PAC to look through its entity donors to the humans behind them.

State corporate law — specifically Delaware, Nevada, and Wyoming LLC law — permits the formation of limited liability companies with no public disclosure of members or ownership. An LLC can be formed in one of these states, receive money from a (c)(4), and spend that money on consultants, vendors, or political expenditures without any public filing that identifies the humans behind the LLC.

None of these laws, on their own, creates the dark-money problem. The problem is the interaction between them. At each rung of the ladder, the disclosure requirement changes. Money that was traceable at Rung 1 becomes untraceable by Rung 4. Each individual law is reasonable in isolation. Stacked, they produce a system in which politically significant activity can be funded without public accountability.

Reformers have proposed closing the stack in various ways — a DISCLOSE Act that would require (c)(4)s to identify donors funding political activity, a rule change that would require PACs to look through entity donors, a federal beneficial-ownership rule for LLCs. None of these proposals has become federal law. The ladder remains intact.

What you can do

This is where the Shadow Patriots section of this module picks up. The citizen action card that accompanies this article will teach you the five-minute entity stack audit — how to take any organization’s name, pull its Form 990 from the ProPublica Nonprofit Explorer, check its Schedule L and Schedule R for related-entity transfers, cross-reference officer lists across related organizations, and identify LLC consultants who receive unexplained lump-sum payments.

The audit is the same mechanism you learned in Module 3 — the ProPublica Nonprofit Explorer is free and public. The information is already there. Most of it is sitting, untouched, on the 990s that the IRS already publishes. The only missing element is the citizen who knows where to look.

You will also get an action card that shows you how to match a (c)(3) and a (c)(4) using shared officer lists, how to flag LLC pass-throughs from public filings, and how to use FEC.gov to look up the disclosed donors of any Super PAC and see whether those donors resolve to humans or to other entities.

We are building this series so that by Module 8, you will be able to look at any political advocacy operation — red, blue, foreign, domestic — and read the architecture in thirty seconds. This module is the second rung of that ladder.

Module 4: CITIZEN ACTION CARD, Open the Russian Doll

The next move

Module 5 will cover Fiscal Sponsorship — the practice of running a political or advocacy operation as a line item inside an established (c)(3), without ever forming a separate organization. Fiscal sponsorship is the move that lets a project bypass the entity formation process entirely and appear as an unmarked program inside a larger, more established nonprofit.

Entity Laddering builds the stack. Fiscal Sponsorship hides the project.

We will map it the same way: mechanism, scale, red case, blue case, citizen action card.

Run the audit. Post what you find. Tag us.

Shadow Patriots. Project Milk Carton. Reach one. Teach one.

Project Milk Carton is a nonpartisan 501(c)(3) public charity (EIN 33-1323547). Case Study A is sourced from PMC Investigation OP-2026-0011 (IRON CURTAIN) — the Leo / Marble Freedom Trust / 85 Fund / DonorsTrust pipeline forensics. Case Study B is sourced from PMC Investigation OP-2026-0005 (EAGLE STRATEGY) and supplemented by published investigative reporting from ProPublica, the Capital Research Center, the New York Times, and public 990 filings. This article has passed SKEPTIC verification (Grade A), THEMIS legal review (cleared), and MINERVA OPSEC review (cleared). Evidence vault hash: see pinned comment.

Read the series: M0 “The Game You Were Never Taught” · M1 “The Tax Code That Became a Battlefield” · M2 “Reading the Map: Decoded” · M3 “The Anonymous Donor” · Visit projectmilkcarton.org

Sources

IRS Form 990: Marble Freedom Trust

IRS Form 990: The 85 Fund / Rule of Law Trust

IRS Form 990: DonorsTrust Inc. and Donors Capital Fund

IRS Form 990: New Venture Fund (EIN 20-5806345)

IRS Form 990: Sixteen Thirty Fund (EIN 26-4486735)

IRS Form 990: Hopewell Fund (EIN 47-4044826)

IRS Form 990: Windward Fund (EIN 46-3600232)

IRS Form 990 Schedule R — Related Organizations (referenced throughout)

FEC Form 3X filings — Super PAC receipts and disbursements (2020–2024 cycles)

Delaware, Nevada, Wyoming Secretary of State corporate filings

OpenCorporates: registered-agent records, LLC formations

OpenSecrets.org: dark-money tracking database (2008–2024 cycles)

Center for Responsive Politics / OpenSecrets: outside spending totals

ProPublica, “The Leonard Leo Network and the $1.6 Billion Anonymous Donation” (reporting on Marble Freedom Trust and the Barre Seid transfer)

New York Times, “How a Dark-Money Network Gained a Foothold in American Politics”

Capital Research Center, “Big Money in Dark Shadows” (Arabella Advisors network documentation)

Capital Research Center InfluenceWatch: Sixteen Thirty Fund, New Venture Fund, Hopewell Fund, Windward Fund profiles

Washington Post and Politico coverage of Sixteen Thirty Fund political spending in the 2020 and 2024 cycles

Congressional Research Service, “Tax-Exempt Organizations: Political Activity Restrictions and Disclosure Rules” (R40183)

Congressional Research Service, “Federal Election Campaign Act: Disclosure Requirements” (R41542)

Internal Revenue Service Exempt Organizations Business Master File (IRS EO BMF)

PMC Investigation: [REDACTED] Arabella network mapping

PMC Investigation: [REDACTED] Marble Freedom Trust, The America Fund / Klingenstein forensics, AFPI Schedule L related-party transactions, Victory Wave LLC opacity analysis, board and personnel overlap matrix